The Risks of Centralized Collateralization in Decentralized Stablecoins and How to Move Forward

The Risks of Centralized Collateralization in Decentralized Stablecoins and How to Move Forward

The USDC depeg and the failure of SVB have impact the whole crypto industry, posing new questions for decentralized stablecoins.

The SVB failure led to the depeg of USDC, the most widely used stablecoins used in the crypto industry, which fell to $0.8788. This had a ripple effect that hit even decentralized stablecoins, that in theory are supposed to be uncorrelated to centralized stablecoins and thus less affected. Frax also fell to $0.87.

This is because $FRAX mainly relies on USDC as collateral.

Black Swan events like this week have tested the value proposition of decentralized stablecoins.

What is the point of holding them if they still suffer from systemic risk?

This article takes Frax as a case study and answers these questions:

Why is Frax backed by USDC?

Is it feasible for decentralized stablecoins to move to fully decentralized collateral while maintaining minimal risk?

There’s no blueprint for the best way to develop decentralized stablecoins.

Frax has risen to fame as the first fractional-reserve stablecoins protocol.

It is open source, permissionless, and fully on-chain.

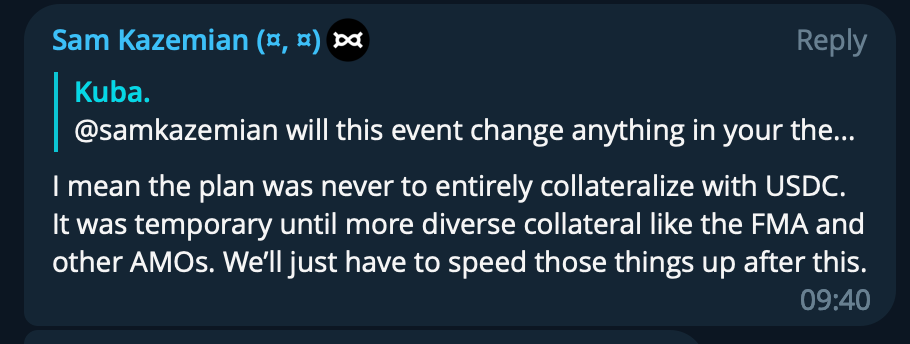

The Frax vision is to become a one-stop-shop for DeFi: a sort of decentralized central bank. As part of their plan, they have recently announced that Frax will raise its collateralization ratio to 100% — following regulatory concerns after the collapse of Terra.

However, as the current USDC depeg has shown us, a CR of 100% is not enough for Frax. The real elephant in the room is which assets should be used as collateral.

This has been an issue that the Frax team, led by Sam Kazemian, was already trying to solve.

Currently, Frax still relies on “tokenized fiat” exposure, as most of the collateral for Frax is composed of USDC.

The range of assets that Frax can leverage as collateral is de facto restricted to:

Real Word Assets (RWA): what MakerDAO is doing for $DAI

Risk-off assets: e.g. USDC;

RWA have for the most part of the bull market dominated the narrative as a fundamental component of stablecoins scaling infrastructure.

There is no right and wrong way to move forward, it all depends on the final vision of the protocol. Since Frax aims to become DeFi’s Central Bank the best way to move forward is not to “take on risky private sector loans”, but rather to focus on the most risk-off assets.

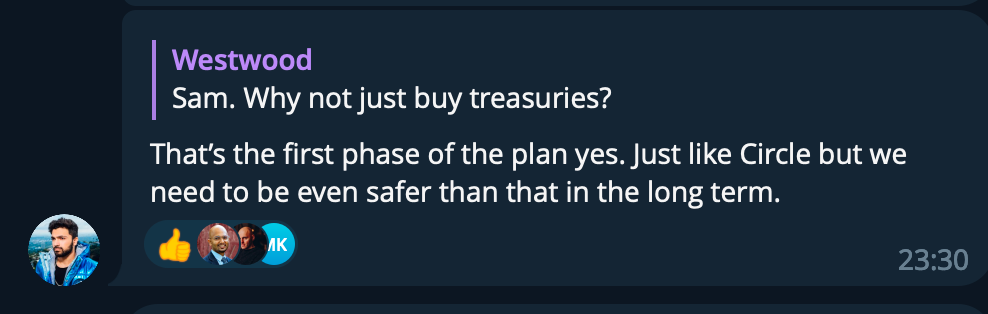

The stablecoin that today looks most like this is Circle USDC, as it is fully backed by US Treasuries. Hence Frax's decision to initially collateralized with USDC, as it is the instrument that “is the less riskiest economical liability of a dollar”.

For instance, if $DAI would be backed by RWA such as Tesla loans, and private companies loans, that would be much riskier than dollar-denominated loans in stablecoins.

Nonetheless, by having most of its collateral as USDC, Frax is not really de-correlated with centralized stablecoins and does not provide any extra level of protection during market turmoils: its faith is linked to Circle and USDC.

Sam acknowledges, of course, the degree of exogenous risk inherent in relying on a centralized third party which eventually materialized this week with the failure of SVB, which impacted Circle and led to USDC depeg.

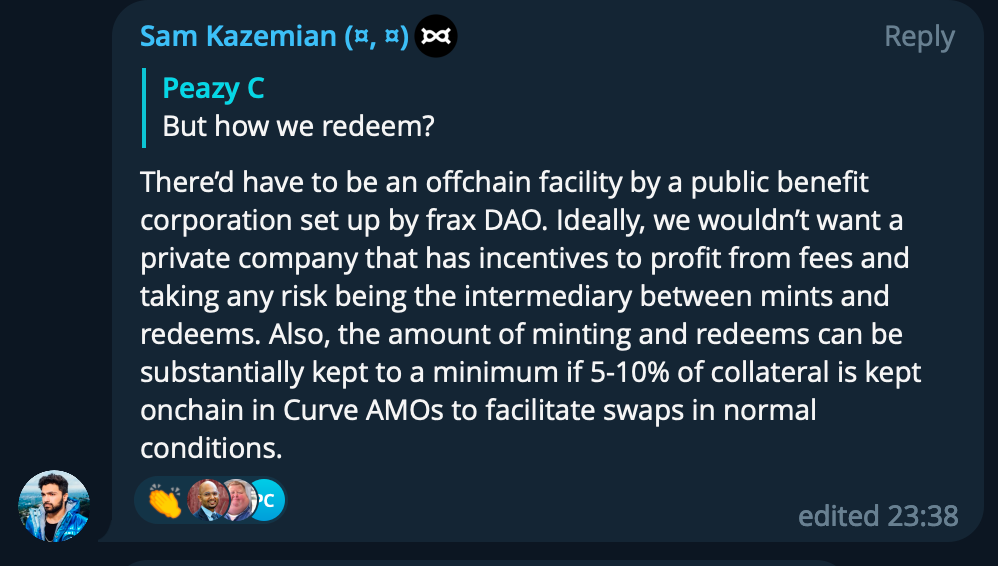

In the words of Sam, there should only be 1 RWA: dollars deposited in a FED master account (FMA). Every large bank can apply to the FED, to deposit dollars directly on its ledger.

Opening an FMA is Frax trump card to solve the Collateralization Dilemma.

There is nothing more risk-free than loans denominated in US dollars by “depositing dollars at the FED’s balance sheet, on the FED’s actual ledger”.

However, as Sam himself has mentioned, this is a long road, full of what-ifs and as such remains pure speculation whether Frax can achieve this or not.

Moving Forward

Frax is a full on-chain entity in the crypto industry. As such the process of getting an FMA will be much harder than for a traditional large bank.

The FED has 6 very strict criteria and 3 different tiers to evaluate whether an entity can get an FMA, given that Frax is a blockchain protocol, it would fall in the higher risk tier, thus receiving progressively more scrutiny before approval.

“The Fed may grant master accounts only to firms that meet the statutory definition of member bank or depository institution, designated financial market utilities, certain government-sponsored enterprises, the U.S. Treasury, and certain official international organizations. For eligible institutions, applicants must be in compliance with relevant laws and regulatory requirements related to payments, anti-money-laundering, sanctions, and risk management, among others; be financially healthy; and not pose risk to the Fed or financial stability”.

During an interview, Sam mentioned that Frax wants to avoid the road paved by Yuga Labs, which recently raised over $1b from a16z. In the words of Sam this introduced “perverse incentives” to reward equity holders and as such would compromise the protocol value proposition and turn Frax into a centralized company. A different way to structure it could be as a non-profit foundation, similar to what Ethereum did.

Obtaining an FMA would ensure that Frax remains decentralized and provides value to its holders, rather than equity holders. What could work in order to scale a leading NFT company (Yuga), would prove destructive for the alignment of interest of a decentralized company aiming to become DeFi Central bank.

A first step in the direction of not relying on USDC has been mentioned by Sam in Frax telegram group: Frax may soon start to purchase US treasuries directly.

Food for Thought

The recent events have battle-tested the crypto ecosystem as a whole. I’d say that Frax has proved to be strong enough, showing resilience and a strategy to improve on their collateral.

This has sped up the process of finding alternative collateral. Buying US treasuries directly could provide to be an initial step in the right direction.

With the recent rollouts of Fraxswap and Fraxlend, Frax has become the first DeFi protocol to offer stablecoin, liquidity, and lending services under one umbrella on Ethereum. By controlling the full stack, Frax is further expanding its ability to conduct arbitrary monetary policy to support its stablecoin.

This is an unpaved road, Frax never had it easy. Aside from collateralization issues, the next few months will also see further progress in US regulation on stablecoins. Truly a make-it-or-break-it moment for Frax.

An extra point here is for the transparency of the communication of Sam and the Frax team. Any doubt? Any issue? Ask and you will be given an answer. I am not sponsored by Frax lol

Food for thought…